India, the world’s fifth-largest economy, is rapidly gaining momentum and is projected to surpass Japan as the third-largest economy in the next five years [1]. With strong GDP growth, manageable inflation, and a healthy consumer base, the nation’s economic outlook remains robust. Supported by rising capital expenditure (capex), favorable demographics, and solid corporate profitability, India is likely poised to play an increasingly prominent role in the global economic landscape.

GDP Growth and Sectoral Shift

India’s GDP is forecast to grow at a steady 6-8% annually, placing it on track to overtake global competitors like Japan by 2029. As seen in the chart below, the service sector remains the dominant force behind this growth, contributing over 60% to the GDP. Unlike other emerging markets, India has taken a non-traditional path by leapfrogging directly into services, which has expanded at a faster pace than both agriculture and manufacturing.

India’s Financial Transformation

The banking sector has undergone substantial reform, highlighted by digitalization and the implementation of bankruptcy laws. Bank lending is on a strong upward trajectory, with India's stock, bond, and private markets growing at a rapid pace. In addition, digital payments through the Unified Payments Interface (UPI) have surged from INR 0.2 trillion in 2019 to INR 20 trillion in 2024.

As the country continues to advance technologically, digital payments and financial inclusion have paved the way for a more accessible and dynamic economy. This boom in digital transactions has strengthened India’s position as a global leader in fintech innovation, making it a key player in shaping the future of financial systems.

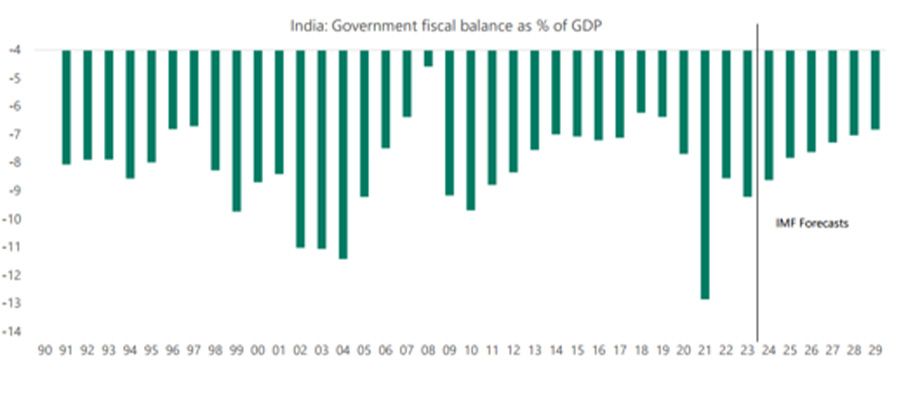

A Favorable Inflation and Fiscal Outlook

Despite global inflationary pressures, India’s core inflation has remained low at 3.6%, well within the central bank’s target range. The government’s fiscal policies have also been prudent, contributing to an improving fiscal balance. This is evident in the sharp improvement in India’s current account balance, which has significantly reduced its deficit over the past decade. The rupee has stabilized, further bolstering economic confidence among investors.

A Growing Workforce

One of India’s greatest strengths is its demographic profile. With a median age significantly lower than other major economies like China, the U.S., and Japan, India boasts a growing working-age population. This young workforce is set to power the country’s future economic trajectory, offering both talent and labor in abundance. As the working-age population grows, the dependency ratio is expected to fall, which could create a favorable environment for sustained economic expansion.

Foreign Investment and Trade

India’s attractiveness as an investment destination continues to rise. Foreign institutional investors and foreign portfolio investors have maintained positive net inflows, while foreign direct investment remains strong. These capital inflows are crucial for funding India’s ambitious infrastructure and growth projects. In addition, the country’s trade sector is witnessing impressive growth, with service exports on a sharp rise. India’s share of global service exports has steadily increased, reinforcing its dominance in the technology and services sectors.

The Path Forward

India's future has the potential to be poised for success, driven by solid economic fundamentals, a resilient financial system, and a youthful, expanding population. As the country accelerates its efforts to fortify its financial and economic frameworks, the coming decade could witness its rise as a key player on the world stage.

How Many Investors Gain Exposure to Companies in the Indian Financial Sector?

The Range India Financials ETF (INDF)

The Range India Financials ETF (Ticker: INDF) seeks to track the performance of Indian banks, financial institutions, housing finance companies, insurance companies, and other financial services companies as measured by the Nifty Financial Services 25/50 Index.

[1] All data sourced from: Apollo Global Management. (October 2024). Outlook for India: Strong GDP growth, low inflation, upbeat consumers and firms. [Charts taken from slide 9,19]

Carefully consider the Funds’ investment objectives, risk factors, charges and expenses before investing. This and additional information can be found in the Fund’s prospectus, which may be obtained by visiting www.rangeetfs.com/indf, or by calling 1-800-617-0004. Read the prospectus carefully before investing.

Investing involves risk, including the possible loss of principal. International investments may also involve risk from unfavorable fluctuations in currency values, differences in generally accepted accounting principles, and from economic or political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume.

The Fund is non-diversified. Its concentration in an industry or sector can increase the impact of, and potential losses associated with, the risks from investing in those industries/sectors.

Investing in India may involve the risk of capital loss from unfavorable fluctuations in currency values, from differences in generally accepted accounting principles, or from economic or political instability in India as well as increased volatility and lower trading volume. Certain restrictions on foreign investment may decrease the liquidity of the Fund’s portfolio, subject the Fund to higher transaction costs, or inhibit the Fund’s ability to track the Index. The Fund’s investments in securities of issuers located or operating in India may be limited or prevented, at times, due to the limits on foreign ownership imposed by the Reserve Bank of India (“RBI”).

The Fund is registered as a foreign portfolio investor (“FPI”) with the Securities and Exchange Board of India (“SEBI”) in order to have the ability to make and dispose of investments in Indian securities. There can be no assurance that the Fund will qualify or continue to qualify as an FPI, or that the Indian regulatory authorities will continue to grant such qualifications and the loss of such qualifications could adversely impact the ability of the Fund to make and dispose of investments in India.

Narrowly focused investments and investments in smaller companies typically exhibit higher volatility. Financial services companies are subject to extensive governmental regulation, which may limit both the amounts and types of loans and other financial commitments they can make, the interest rates and fees they can charge, the scope of their activities, the prices they can charge and the amount of capital they must maintain. There is no guarantee the fund will achieve its stated objective.

A new or smaller fund is subject to the risk that its performance may not represent how the fund is expected to or may perform in the long term. In addition, new funds have limited operating histories for investors to evaluate and new and smaller funds may not attract sufficient assets to achieve investment and trading efficiencies.

Shares are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. The market price returns are based on the official closing price of an ETF share or, if the official closing price isn’t available, the midpoint between the national best bid and national best offer (“NBBO”) as of the time the ETF calculates current NAV per share, and do not represent the returns you would receive if you traded shares at other times. NAVs are calculated using prices as of 4:00 PM Eastern Time.

Exchange Traded Concepts, LLC serves as the investment advisor of the fund. The Fund is distributed by SEI Investments Distribution Co. (SIDCO, 1 Freedom Valley Drive, Oaks, PA 19456), which is not affiliated with Exchange Traded Concepts, LLC, or any of its affiliates.